If you suffered a devastating loss to one of your buildings, do you have peace of mind that the sums insured on your current insurance programme are sufficient to rebuild your building back to its pre-loss condition? The vast majority of businesses in the UK would respond ‘no’ to this question.

Past claims

A quick search online will yield a plethora of incidents where a sporting organisation has suffered a catastrophic incident, such as a fire destroying one of their buildings.

The buildings sum insured is brought into question in situations like this, or even when a building is not completely destroyed but suffers damage. What would happen if your sum insured was insufficient at the time of a claim?

Consequences of under-insurance

Because of the current high rates of inflation, strains on supply chains, and labour shortages, rebuilding is becoming more expensive and time-consuming.

These are crucial factors to take into account when choosing the Indemnity Period under your Business Interruption cover. The Indemnity Period determines the length of time Business Interruption losses are paid.

Another significant concern is the ‘Average’ clause which is found on almost every single commercial insurance policy.

In the event of a claim, if there is any under-insurance present at the time, ‘Average’ would reduce any claims payment by the percentage of under-insurance. This could have disastrous consequences for you. The following hypothetical example will let you see the potential effects.

A building is insured for £1,000,000, however at the time of the loss it is deemed that the true value of the building is £1,500,000. The client suffers fire damage resulting in a loss of £250,000. The following calculation is then made to work out how much of the claim insurers will pay.

The client would only receive 66% of the total cost, leaving them to find just over £83,000 to put them back in the same position as before.

Not only would you be faced with having to find a significant amount of money, your business would be disrupted for a longer amount of time, the cost of temporary accommodation would increase, and if you rented out any space in one of your buildings you would be without rental income; potentially even losing the tenant. These are only a few of the issues you could be faced with.

Solution to under insurance

Howden Insurance Brokers are acutely aware of the risks associated with incorrectly insuring your buildings. We also recognise that it may have been some time since your buildings were last valued. When determining the true rebuild costs of a building there are numerous factors to consider, which can only be done by a qualified individual.

We work in partnership with four companies who are experts in this field and can provide our clients with a detailed report and reinstatement figure for their buildings. This would bring clarity to the correct and current sums insured, as well as provide you peace of mind knowing that you will not be affected by ‘Average’ in the event of a claim.

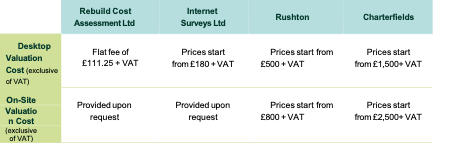

These companies can offer either a ‘desktop valuation’ or an ‘on-site valuation’.

A ‘desktop valuation’ is significantly less expensive as there is no requirement for a surveyor to visit your premises. They will carry out the survey internally using various tools and software, along with any additional information you provide.

An On-Site Valuation is more accurate as a surveyor will visit your premises to determine the rebuild figures. The four companies and their associated costs are briefly summarised in the table below.

Rereference: BIBA (2022) BIBA Works with Allianz To Create A New Guide To Help Reduce The Risk of Underinsurance. Available at: https://www.biba.org.uk/press-releases/biba-workswith-allianz-to-create-a- new-guide-to-help-reduce-the-risk-of-underinsurance/ (Accessed 19 July 2022).

Please do not hesitate to contact the Howden Golf Team on [email protected] if you wish to discuss this further.